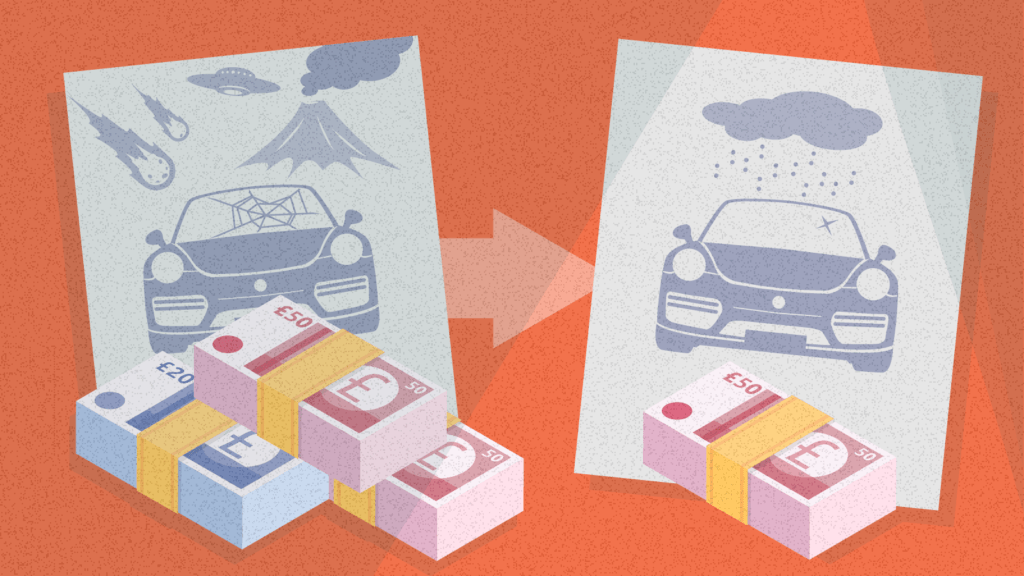

Case Study: An Insurance Company Reduced Fraud by 36% with Clever Messaging Rooted in Psychology

In this case study, you’ll discover:

- How you can apply nudging to reduce opportunistic fraud; and

- How Dectech achieved an average 36% decrease in fraud with clever messaging.

Unlock to continue reading.

Unlock this case study – 9,90€, or

all 60+ case studies – 149€

Or get lifetime access to all of InsideBE for 790€ here.